Thwarted investment possibility for 🇺🇸 expats

IRS rules make a popular investment tool too pricey for most 🇺🇸expats

Photo by Rebekah Howell on Unsplash

Grandma was right

ETF is an abbreviation for Exchange Traded Fund, which certainly does not quicken one’s pulse. It might if you’re a busy middle-class person who wants to create an investment nest egg.

ETFs solve a big problem for the middle-class investor: how to diversify even if you’re not rich.

Diversification is investment speak for Grandma’s advice: “Don’t put your eggs in one basket.” Instead of betting all your investment money on one company you spread smaller bets across many companies. It’s unlikely all will simultaneously do badly so your risk is minimized.

The use of diversification to reduce risk is part of Modern Portfolio Theory, which won its author a Nobel Prize in 1990. Grandma didn’t get enough credit.

It used to be very expensive to follow Grandma’s advice

Before ETFs and their mutual-fund predecessors, an investor bought individual company’s shares in 100-share batches.

If a company's shares were trading at $35/share, you had to buy a 100-share lot for $3500 and pay $25 in fees to make the purchase. Selling cost another $25.

Such trading requirements and high transaction costs made diversification too expensive for middle-class investors. Investing in as few as 10 companies would’ve easily required $25,000.

Mutual funds, a precursor to ETFs, made diversification more accessible. Mutual fund managers would buy a whole basket of stocks and bundle them into a single fund share comprising many fractional shares of multiple stocks.

Though mutual funds were a step towards inexpensive diversification, the fees were pretty high and transactions were slow. You had to call or write the mutual fund company, and they then would execute the transaction.

ETFs improved on mutual funds

ETFs turned a basket of company stocks into a single stock that could be bought and sold easily and cheaply through an online broker. Like mutual funds, owning a share of an ETF meant that you owned parts of a lot of companies – diversification in action.

Moreover, ETF fees are very low, 1 or 2%, and much less than mutual fund fees. These efficiencies mean that an investor of very modest means can buy a few ETF shares to get a highly diversified portfolio at a very low cost.

The ETF problem for 🇺🇸 expats

To invest in 🇺🇸 ETFs and similar products, you need to have a brokerage account. Brokers who trade on US stock exchanges restrict their clients to those who live in the US. Tough luck, expat.

Even though most expats have no 🇺🇸 address and can’t trade 🇺🇸 ETFs they could just buy an ETF in the country where they reside. “Eureka!” I thought.

So, as a Canadian resident I bought a couple of Canadian ETFs traded on the Toronto exchange. My diversification problem was solved, or so I thought.

All was good until my expensive cross-border-savvy accountant shared some bad news.

The IRS treats a non-🇺🇸 ETF as a foreign ETF, and foreign is suspect in the eyes of the IRS.

The US Treasury seems to suspect that tax fraud is rampant among expats. So lots of details of your non-🇺🇸 ETF must be included on a Form 8621, which you file with your 1040 tax return. Worse, that 8621 form has to be filed every year that you own a foreign ETF.

You really don’t want to complete Form 8621

An accountant could complete the 8621, but it may cost you $250 just for that form. DIY? No way! Form 8621 is inexplicable to the non-professional.

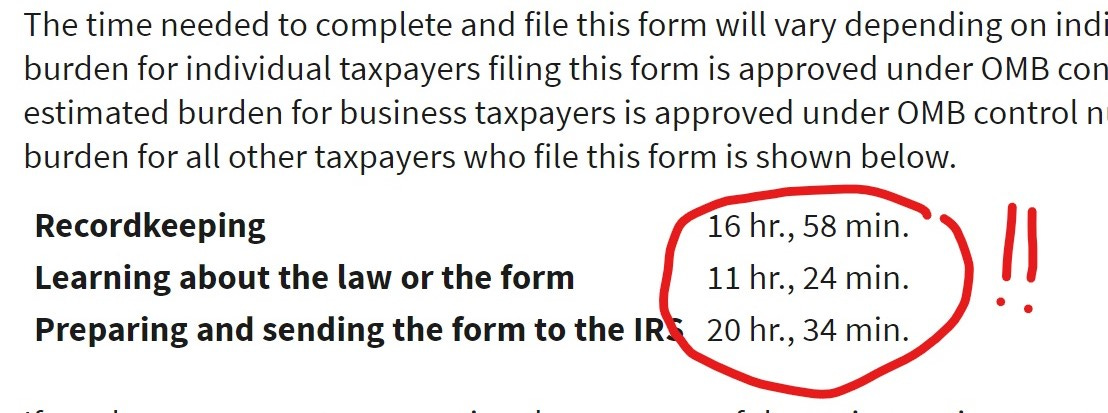

Below is the IRS’ estimate of how long it will take you to complete an 8621.

Just look at the instructions and you’ll call an accountant. You’ll also see why they charge so much.

8621 Bottom line

The annual tax-prep costs in terms of your time or accountant fees for completing a Form 8621 for an ETF are excessive.

You would need to make a large investment in an ETF to make a $250 accountant’s bill or your hours of time worthwhile.

But there’s hope

There are ways an expat investor of modest means can benefit from ETFs as an expat, but they take more explanation. More on this topic in next week’s newsletter.

If you haven’t already subscribed to 🇺🇸 Expat Lessons Learned, please do so below. Then you won’t miss next week’s big reveal.